Hank Sienzant

-

Posts

127 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Store

Posts posted by Hank Sienzant

-

-

HS :You're trying to salvage the money order argument by changing the subject to other things you question.

That is pure baloney from both an intellectual and a forensic angle.

Again, refer to the infamous exhibit CE 399. Which DVP and Hank--the McAdams' poster--ran away from. To me that is a very good comparison. The WC used the rifling marks on CE 399 to cinch the case that this was the bullet that hit Kennedy and Connally. Well, I don't think they believed it. But to someone who just read the report without doing any other research, then yes it made sense.

Until you analyzed the whole one day journey of CE 399.

http://www.ctka.net/2010/journeyCE399.html

You cannot separate out one single part of the transaction from the rest of the multi steps in that same transaction. Just like you cannot ignore the work of other authors and make Armstrong the sole focus of the debate. Like I said, this is a dodge. Coming from people who do not know anything about the work of the other authors. For example:

1. If its the wrong rifle, then how can the transaction be genuine?

2. If Oswald never picked up the rifle, then how can the transaction be genuine?

3. If the postal regs actually prohibited Oswald from picking up the rifle, how can the transaction be genuine?

4. If there is written certification Oswald was at work all day, then how can the transaction be genuine?

5. If the rifle Marina saw did not have a scope on it, then how can the transaction be genuine?

And I could go on and on in this regard. And we can argue about this most current debate also. Everything that Sandy has presented indicates that the bank should have stamped that PMO. And this includes the two bank executives that John and I talked to.

But that is how rabid and unbalanced the other side gets in this particular debate. In any other case, rational people understand that when you pile up anomaly onto anomaly until you have like seven or eight of them in just one transaction, it is simply illogical to say well look at this--the rifling marks--it makes all the other stuff go away. Oswald killed Kennedy.

No it does not make it all go away. And for a lawyer to say the contra when he knows in a court of law all of this would have been in play and witness after witness would have been called to say so, I mean that is just really incomprehensible to me.

The deduction should be the opposite. Unless of course you post at McAdams' site, like Hank. Then you leave the logic outside the door. Its a requirement to post there.

PS: As for Tommy, the droll, as I said before, if you have nothing of substance to offer, then just don't say anything.

Still changing the subject from the money order and now to the rifle bullet. That's a LOGICAL FALLACY known as a red herring.

Already pointed it out. I don't know why you persist. Here, let's go into a bit more detail.

http://www.nizkor.org/features/fallacies/red-herring.html

Description of Red Herring

A Red Herring is a fallacy in which an irrelevant topic is presented in order to divert attention from the original issue. The basic idea is to "win" an argument by leading attention away from the argument and to another topic. This sort of "reasoning" has the following form:

1.Topic A is under discussion.

2.Topic B is introduced under the guise of being relevant to topic A (when topic B is actually not relevant to topic A).

3.Topic A is abandoned.

This sort of "reasoning" is fallacious because merely changing the topic of discussion hardly counts as an argument against a claim.

And of course, your argument that "Unless of course you post at McAdams' site, like Hank. Then you leave the logic outside the door" is simply the LOGICAL FALLACY of ad hominem. That's where you attack the messenger, instead of the message.

http://www.nizkor.org/features/fallacies/ad-hominem.html

Description of Ad Hominem

Translated from Latin to English, "Ad Hominem" means "against the man" or "against the person."

An Ad Hominem is a general category of fallacies in which a claim or argument is rejected on the basis of some irrelevant fact about the author of or the person presenting the claim or argument. Typically, this fallacy involves two steps. First, an attack against the character of person making the claim, her circumstances, or her actions is made (or the character, circumstances, or actions of the person reporting the claim). Second, this attack is taken to be evidence against the claim or argument the person in question is making (or presenting). This type of "argument" has the following form:

1.Person A makes claim X.

2.Person B makes an attack on person A.

3.Therefore A's claim is false.

The reason why an Ad Hominem (of any kind) is a fallacy is that the character, circumstances, or actions of a person do not (in most cases) have a bearing on the truth or falsity of the claim being made (or the quality of the argument being made).

My message was on the topic of the money order and whether it appears valid from the contents of the money order itself. I see you didn't bother to respond on that subject whatsoever. Instead, you bring up some supposed other 'anomalies' in an attempt to change the subject.

Happy Holidays to you and yours,

Hank

PS: I haven't posted at McAdams site for about a year. Besides, that's just another LOGICAL FALLACY known as "poisoning the well". You point that out (that I've posted at McAdams site) as if it's a negative, and that's the very definition of poisoning the well, Jim. I've posted at a lot of sites, Jim - going back to CompuServe, Prodigy, and the old AOL bulletin boards.

http://www.nizkor.org/features/fallacies/poisoning-the-well.html

Description of Poisoning the Well

This sort of "reasoning" involves trying to discredit what a person might later claim by presenting unfavorable information (be it true or false) about the person. This "argument" has the following form:

1.Unfavorable information (be it true or false) about person A is presented.

2.Therefore any claims person A makes will be false.

This sort of "reasoning" is obviously fallacious. The person making such an attack is hoping that the unfavorable information will bias listeners against the person in question and hence that they will reject any claims he might make. However, merely presenting unfavorable information about a person (even if it is true) hardly counts as evidence against the claims he/she might make.

Good luck getting anyone to fall for this kind of argument, Jim.

-

And let me add this other point which Lance and his buddy DVP are busy distorting--this work was not all based on Armstrong.

That is an adulteration of the record. There are at least four other sources for this rifle debate: the late Ray Gallagher, Jerry McLeer, David Josephs and Gil Jesus.

Ray is the first guy who intimated something was wrong with the transaction: How could the money order do all of that in 24 hours. That is go from Dallas to Chicago to the bank and be deposited all in a day.

McLeer has some interesting exhibits on his site showing there was more than one rifle in evidence.

Gil has done some really fantastic work on tracing the delivery all the way from Italy to Chicago. That work is really kind of revolutionary showing that the rifle in evidence could not have been the one ordered.

And David just did a two part article at CTKA, which also questions the provenance of the rifle in the BYP, among several other points.

So to say that this is all Armstrong about the rifle, that is simply not the case. Its a form of intellectual dishonesty. And I think its done for personal reasons and also to limit the scope of the debate.

Which is what they always try and do.

Ray is the first guy who intimated something was wrong with the transaction: How could the money order do all of that in 24 hours. That is go from Dallas to Chicago to the bank and be deposited all in a day.

Sorry, you need to provide evidence, not just intimation, that there's anything wrong with the transaction.

McLeer has some interesting exhibits on his site showing there was more than one rifle in evidence.

Sorry, changing the subject from the money order to the rifle won't work. We understand that's a logical fallacy, and we understand why you're trying this.

Gil has done some really fantastic work on tracing the delivery all the way from Italy to Chicago. That work is really kind of revolutionary showing that the rifle in evidence could not have been the one ordered.

Sorry, changing the subject from the money order to the rifle won't work. We understand that's a logical fallacy, and we understand why you're trying this.

And David just did a two part article at CTKA, which also questions the provenance of the rifle in the BYP, among several other points.

You understand the subject matter under debate is the money order? Why are you trying to derail the argument to the rifle at this time? For one reason only, you understand the money order is a lost cause. So now you're trying to do what all conspiracy theorists do, deflect the argument to other points. If you want to discuss the rifle, start a new thread, or contribute to one of the several dozens or hundreds on the rifle you can find on this forum.

So to say that this is all Armstrong about the rifle, that is simply not the case.

We know. It's about the money order. You're the only one making it about the rifle.

Its a form of intellectual dishonesty.

We agree! We just disagree on whose intellectual dishonesty.

And I think its done for personal reasons and also to limit the scope of the debate.

Arguing every point at once isn't very feasible. So yeah, the debate has to be limited if it's going to go anywhere. Right now, it's limited to the question of the money order, and whether there's anything wrong with it. That has not be demonstrated, despite Sandy's best efforts. You want to change the subject from the money order to the rifle because you can see Sandy isn't getting where he'd like to go.

We understand, Jim.

Hank

-

Lance Payette's best friend has turned out to be David Von Pein.

As they say Birds of a Feather.

As for, let us call it, Payette's complaint, about where has everyone else gone; as I noted many moons ago, for reasons of time and psychology, I refuse to get into a constant back and forth with DVP anymore. It is simply stupid to argue with a zealot.

Sandy is doing us all a very good service by arguing with them both. Bless him on this holiday season.

As for me, I go back to my original argument: if everything about a transaction is dubious, from A to Z, it is illogical to assume that one last step in the process is genuine. And that is what DVP and Payette want you to believe. Which is why they avoid almost everything else. In fact they do not even want to bring it up. But from Oswald's time cards covering everything that morning, to the fact that no one admits giving him the rifle, and that the postal regs would not allow him to get the rifle--and every step in between--this evidentiary trail is bogus.

Including THE FACT THAT ITS THE WRONG RIFLE!! Yet DVP and his new buddy want us to buy iinto the proposition that OK, so what with all that? Let us forget all of that: we have the UFC!

To me this is like saying well look, there is the exhibit CE 399 and it has the identifying rifle marks on it. Therefore, Oswald killed Kennedy, let us go home.

Thank God we did not buy that piece of snake oil.

But yet, this is exactly what Lance said many pages ago on this thread about the PMO. It has that number on it, let us go on.

Everything else smells, but this makes it all a rose garden. Some indefatigable lawyer.

Thanks Sandy. Have a good Xmas.

You're trying to salvage the money order argument by changing the subject to other things you question.

Sorry, that's illegitimate argument... it's a logical fallacy known as a red herring to bring up the rifle at this time when the subject is, in fact, the money order.

Hank

-

Hank,

Endorsements have more than one purpose. One is the guaranty that you point out is considered to be in place regardless of whether or not an express guaranty is included in the endorsement. Another purpose is to indicate the ABA and address of the sending bank. It is apparently for non-guaranty purposes that the bank endorsement is required.

BTW, keep in mind that whatever you interpret from that paragraph in the FRB operating circular, it will be applicable not only to postal money orders but to checks as well. Don't you remember way back when, when we were all young, that virtually every check had bank endorsements stamped on them? According to the operating circular cited, the same should have been true of PMOs as well. (Though, beginning with the PMOs of 1963, an FRB stamp appeared on the front side of the PMO in the form of a file locator number. This may well have been the only FRB stamp to appear on those PMOs. We don't know for certain.)

Are you saying checks don't require bank endorsements any more, Sandy? If that's true, perhaps you might want to consider why they don't.

It looks like we might finally be beginning to head in that direction, now that people can deposit checks by sending a photo of it over the Internet. Think about it... how does a bank stamp a photograph? But we may NOT be heading in that direction. I say that because I saw some of my checks that appeared to have been sent from a local bank to a national one via photo, and they actually had bank endorsements photographically applied to their backs. I could tell that the stamping was done photographically because the background of the "photo-stamp" covered up text that is printed on the back side of the checks.

In fact, as I understand it, you don't even have to stand in line and deposit a check anymore. You can just submit a photo of your check to the bank, and that will work as well. Imagine that.

Now, in the early 1960's, what changed in regards to postal money orders, and why?

The US government was (slightly) ahead of the technological curve. They chose hole-punching as a way of making computer automation possible. This began around 1958. Meanwhile, around the same time, the ABA introduced the magnetic ink standard that banks still use today. (Maybe you've noticed the futuristic-looking numbers printed at the bottom of checks. They are printed with magnetic ink that can be read by machines.) I think it was in the 1970s that the US government switched PMOs over to the magnetic ink standard.

Wasn't the whole point of the changes to be able to bulk-process money orders, rather than manually handle each one, to speed up transaction times? Wasn't it to get people out of the loop and let the computers do it? Hence the IBM punch-card format, so that the information on the money order was machine-readable?

What's the point of putting in all these changes to make them machine-readable and speed up processing time ....

I don't know. But bank endorsement is still being done, even on photographically sent items.

if you're still going to process them manually, and hand-stamp them every step of the way?

They aren't processed and stamped manually. It is done by machine.

Hank

And that takes us back to the number at the top of the postal money order in question, doesn't it?

Why is anything else necessary to establish this went to the FRB exactly as it should have?

We have a hand-stamp that was applied manually to start the process.

We have the machine applied number that denotes the money order made it through the FRB system okay.

Analogy hunting is not the name of the game. That worked 50 years ago for the Mark Lanes, Harold Weisbergs, and Sylvia Meaghers of the world to sell books. But it's not sufficient to establish a conspiracy. In fact, it's a logical fallacy to assert that these kinds of supposed anomalies establish anything, let alone a conspiracy.

http://www.theskepticsguide.org/resources/logical-fallacies

Anyone asserting that the absence of bank stamps; or that the doorman image in the Altgens photo; or the price of the rifle being wrong in the earliest reports; or any of about one hundred thousand other supposed anomalies; is a smoking gun that establishes a conspiracy is simply wrong, and invoking a logical fallacy to boot:

Confusing currently unexplained with unexplainable

Because we do not currently have an adequate explanation for a phenomenon does not mean that it is forever unexplainable, or that it therefore defies the laws of nature or requires a paranormal explanation. An example of this is the “God of the Gaps” strategy of creationists that whatever we cannot currently explain is unexplainable and was therefore an act of god.

Hank

-

But, Hank, it says in that very same paragraph of the regulation that....

"The endorsement of the sending bank should be dated and should show the American Bankers Association transit number of the sending bank in prominent type on both sides."

None of which is found on the CE788 Hidell money order.

But it's very likely (IMO) that the Hidell M.O. was part of a bulk transfer of postal money orders which was accompanied by a cash letter (deposit ticket), which very likely did have those stamps on it (i.e., the date and the ABA transit numbers).

To believe the Hidell M.O. is fraudulent is silly, especially when we KNOW it was found just exact where it should have been found in Alexandria/Washington.

And we also have information in CD75 coming from a First National Bank Vice President (Wilmouth) verifying that First National DID handle the $21.45 Postal Money Order in question.

How many more years will conspiracy theorists completely ignore these important paragraphs found in Commission Document No. 75? ....

The paragraph I am looking at says all that's necessary is an endorsement TO the bank. And we have that in the Kleins stamp.

It goes on to say that "The act of sending or delivering a cash item to us or to another Federal Reserve Bank will, however, be deemed and understood to constitute a guaranty of all prior endorsements on such item, whether or not an express guaranty is incorporated in the sending bank’s endorsement."

In other words, the FRB will accept money orders without any additional endorsements, and it's understood that the very act of submitting the money order for payment is the guarantee that the prior endorsements are valid on the part of the submitting bank (in this case, The First National Bank of Chicago.

Endorsements

13. All cash items sent to us, or to another Federal Reserve Bank direct for our account, should be endorsed without restriction to the order of the Federal Reserve Bank to which sent, or endorsed to the order of any bank, banker or trust company, or with some similar endorsement. Cash items will be accepted by us, and by other Federal Reserve Banks, only upon the understanding and condition that all prior endorsements are guaranteed by the sending bank. There should be incorporated in the endorsement of the sending bank the phrase, “ All prior endorsements guaranteed.” The act of sending or delivering a cash item to us or to another Federal Reserve Bank will, however, be deemed and understood to constitute a guaranty of all prior endorsements on such item, whether or not an express guaranty is incorporated in the sending bank’s endorsement. The endorsement of the sending bank should be dated and should show the American Bankers Association transit number of the sending bank in prominent type on both sides.

You are correct that the money order doesn't have any additional endorsements. But per the language above, I'm not seeing where it needs any, as the very act of submitting the money order for payment is the guaranty that the sending bank (in this case, First National of Chicago) guarantees the item is valid.

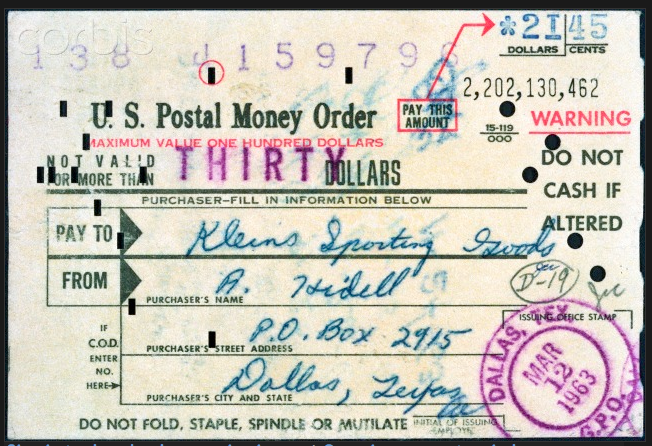

Could the ABA number be the number specified on the Klein's stamp ("50 91144") right under the bank name?

It appears the FIRST NATIONAL BANK OF CHICAGO no longer exists.

http://www.nndb.com/company/096/000124721/

Hank

Hank,

Endorsements have more than one purpose. One is the guaranty that you point out is considered to be in place regardless of whether or not an express guaranty is included in the endorsement. Another purpose is to indicate the ABA and address of the sending bank. It is apparently for non-guaranty purposes that the bank endorsement is required.

BTW, keep in mind that whatever you interpret from that paragraph in the FRB operating circular, it will be applicable not only to postal money orders but to checks as well. Don't you remember way back when, when we were all young, that virtually every check had bank endorsements stamped on them? According to the operating circular cited, the same should have been true of PMOs as well. (Though, beginning with the PMOs of 1963, an FRB stamp appeared on the front side of the PMO in the form of a file locator number. This may well have been the only FRB stamp to appear on those PMOs. We don't know for certain.)

Are you saying checks don't require bank endorsements any more, Sandy? If that's true, perhaps you might want to consider why they don't.

In fact, as I understand it, you don't even have to stand in line and deposit a check anymore. You can just submit a photo of your check to the bank, and that will work as well. Imagine that.

Now, in the early 1960's, what changed in regards to postal money orders, and why?

Wasn't the whole point of the changes to be able to bulk-process money orders, rather than manually handle each one, to speed up transaction times? Wasn't it to get people out of the loop and let the computers do it? Hence the IBM punch-card format, so that the information on the money order was machine-readable?

What's the point of putting in all these changes to make them machine-readable and speed up processing time if you're still going to process them manually, and hand-stamp them every step of the way?

Hank

-

In neither case did the person say anything had been proven.

Right on the Armstrong website the following statement is made regarding the bleed-thru:

"NOTE: Serious researchers should be focusing attention on the inked postal stamps that appear on the front of the money order (Dallas, TX, Mar 12, 1963), the inked endorsement stamp (Klein's) and the inked initials and dates that appear on the back of this money order. An explanation is needed as to how ink from the postal stamp and ink from the initials/dates can "bleed" thru to the other side of the money order. Postal money orders were made from card stock similar to an index card or an IBM type punch card--between 90# and 110# paper. This paper stock was crisp, firm, and ink "bleed-thru" to the reverse side was virtually impossible. I don't understand why or how ink "bleed-thru" occurred on CE 788. The original postal money order disappeared long ago, and only FBI photographs of CE 788 remain. Who authorized and/or caused the disappearance of the original money order is unknown. Only black and white photographs remain. This ink "bleed-thru" deserves a valid explanation."

Armstrong said, "This ink 'bleed-thru' deserves a valid explanation." And now we have it.

No claim was made by Armstrong other than the bleed-thru appearing to show that CE 788 was not original card stock.And the claim was factual at the time.

Armstrong obviously didn't research this very well, or else he would have discovered the answer in the Warren Commission testimony, as cited previously here by DVP, wouldn't he?

There's the rub. I see a lot of allusions to Armstrong's research, but if he couldn't even discover why there was bleed through, then that calls into question how great a researcher he really is.

Doesn't it?

Hank

The paragraph about ink bleeding on the money order isn't in Armstrong's book. It does appear on his website, clearly as an afterthought. And if you read the paragraph you will see that he doesn't claim to have researched it, because he urges "serious researchers" to do so.

The quote I saw was:

"The "bleed-thru" of the ink is a strong indication that postal money order 2,202,130,462, shown as CE 788, was not original card stock." -- John Armstrong

That is wrong.

Right?

Hank

It is incorrect to state that the bleed-thru was due to the postal money order being printed on paper thinner than the original card stock that PMOs at the time were printed on. The bleed-thru was instead caused by a chemical bath that was used for detecting fingerprints.

That was testified to by a witness before the WC. I forget the man's name.

Here is video that shows the process:

http://science.wonderhowto.com/how-to/reveal-latent-fingerprints-paper-other-surfaces-302464/

Ok, that's what I was going for.

Hank

-

Armstrong obviously didn't research this very well, or else he would have discovered the answer in the Warren Commission testimony, as cited previously here by DVP, wouldn't he?

There's the rub. I see a lot of allusions to Armstrong's research, but if he couldn't even discover why there was bleed through, then that calls into question how great a researcher he really is.

Doesn't it?

Hank

The paragraph about ink bleeding on the money order isn't in Armstrong's book. It does appear on his website, clearly as an afterthought. And if you read the paragraph you will see that he doesn't claim to have researched it, because he urges "serious researchers" to do so.

The quote I saw was:

"The "bleed-thru" of the ink is a strong indication that postal money order 2,202,130,462, shown as CE 788, was not original card stock." -- John Armstrong

That is wrong.

Right?

Hank

Hank,

DVP and I already had a mini-debate over the use of the words like "appears" and "indicates." If you care to read the debate, it begins at post 295 on this page:

http://educationforum.ipbhost.com/index.php?showtopic=22439&page=20

I saw that. Is it a strong indication of "not original card stock", as Armstrong suggests, given what you know now?

Hank

-

5) It does not appear that the PMO in Evidence even has a new 9-digit ABA routing # or the older ####-#### 8-digit format. What's the ABA for this PMO Dave?

It's right there next to the WARNING.. 15-119/000 ... in the old style format.

Hank

-

Could the ABA number be the number specified on the Klein's stamp ("50 91144") right under the bank name?

William Waldman testified that that number was the Klein's "account number". Whether or not some of those numbers signify "ABA transit numbers", I have no idea....

ABA transit (routing) numbers are nine digits. The Klein's account number would bear no relation to an ABA transit number. A PMO, unlike a check, is drawn on the Post Office rather than a bank. All national banks must be members of the Federal Reserve system; state-chartered banks may join but do not have to. When a PMO was presented to a Federal Reserve member bank like FNB in Chicago, the PMO wasn't going to pass through any further stages - it was simply going to the regional Federal Reserve Bank for the region in which the member bank was located, to be processed by the FRB as the agent for the Post Office. The Federal Reserve regulations basically said, "If the Post Office has a problem with a PMO after we process it, that will be the Post Office's problem and we are not going to become involved." I am out of my depth, as is everyone else on this thread, but it is difficult for me to see any reason the Federal Reserve would require an endorsement by a member bank that was simply transmitting a PMO to the regional FRB. As Hank has stated, the Klein's endorsement was sufficient to show how/why the PMO was in the hands of the Chicago bank. My guess is that it is a fundamental error to equate a PMO to a bank check.

Lance,

I've also always felt that it was an error to compare a personal check with a post office money order.

They are fundamentally different financial instruments. A personal check is written by a person and drawn on that person's issuing bank account. It is backed by only the money in the account. That account could have no money in it, and the check will then bounce once it gets back to the issuing back and is reconciled against the account. They will get their money back from whomever presented it to the bank, and ultimately, it will fall upon the check-writer (or the first person to deposit the check, if the check-writer can't be located) to repay that money. That's why you shouldn't fall for scams promising you 10% for writing checks for someone in Nigeria, even when they send you a check for the money upfront...

A post office money order is entirely different. The post office gets the money up front, and thereafter issues the money order. It's already guaranteed good by the post office, and you can accept that with no fear the money order will bounce.

I always believed it was an error on Armstrong's part to compare the two, and argue that since a personal check needs bank stamps every step of the way, so would a post office money order.

It's like comparing pineapples and hand grenades.

Hank

-

David, thanks for the info.

You are correct, the "50 91144" number on the postal money order Klein's stamp is the account number of Kleins at the First National Bank of Chicago. It's not the ABA routing number as I surmised it might be.

Hank

-

But, Hank, it says in that very same paragraph of the regulation that....

"The endorsement of the sending bank should be dated and should show the American Bankers Association transit number of the sending bank in prominent type on both sides."

None of which is found on the CE788 Hidell money order.

But it's very likely (IMO) that the Hidell M.O. was part of a bulk transfer of postal money orders which was accompanied by a cash letter (deposit ticket), which very likely did have those stamps on it (i.e., the date and the ABA transit numbers).

To believe the Hidell M.O. is fraudulent is silly, especially when we KNOW it was found just exact where it should have been found in Alexandria/Washington.

And we also have information in CD75 coming from a First National Bank Vice President (Wilmouth) verifying that First National DID handle the $21.45 Postal Money Order in question.

How many more years will conspiracy theorists completely ignore these important paragraphs found in Commission Document No. 75? ....

The paragraph I am looking at says all that's necessary is an endorsement TO the bank. And we have that in the Kleins stamp.

It goes on to say that "The act of sending or delivering a cash item to us or to another Federal Reserve Bank will, however, be deemed and understood to constitute a guaranty of all prior endorsements on such item, whether or not an express guaranty is incorporated in the sending bank’s endorsement."

In other words, the FRB will accept money orders without any additional endorsements, and it's understood that the very act of submitting the money order for payment is the guarantee that the prior endorsements are valid on the part of the submitting bank (in this case, The First National Bank of Chicago.

Endorsements

13. All cash items sent to us, or to another Federal Reserve Bank direct for our account, should be endorsed without restriction to the order of the Federal Reserve Bank to which sent, or endorsed to the order of any bank, banker or trust company, or with some similar endorsement. Cash items will be accepted by us, and by other Federal Reserve Banks, only upon the understanding and condition that all prior endorsements are guaranteed by the sending bank. There should be incorporated in the endorsement of the sending bank the phrase, “ All prior endorsements guaranteed.” The act of sending or delivering a cash item to us or to another Federal Reserve Bank will, however, be deemed and understood to constitute a guaranty of all prior endorsements on such item, whether or not an express guaranty is incorporated in the sending bank’s endorsement. The endorsement of the sending bank should be dated and should show the American Bankers Association transit number of the sending bank in prominent type on both sides.

You are correct that the money order doesn't have any additional endorsements. But per the language above, I'm not seeing where it needs any, as the very act of submitting the money order for payment is the guaranty that the sending bank (in this case, First National of Chicago) guarantees the item is valid.

Could the ABA number be the number specified on the Klein's stamp ("50 91144") right under the bank name?

It appears the FIRST NATIONAL BANK OF CHICAGO no longer exists.

http://www.nndb.com/company/096/000124721/

Hank

-

I have a idea for you Lance.

Given that FRB requirements for PMO clearing hasn't changed much since 1960, maybe the Agreement between the U.S. Postal Service and Federal Reserve Banks hasn't changed much either. If you want to prove me wrong about the Agreement being published in operating circulars, just find the current agreement and show me that it contains regulations for commercial banks that aren't in the operating circulars. Also, you could show me that the Agreement has an exemption for bank endorsements on PMOs.

It shouldn't be too hard to find the current Agreement. Tom Scully could probably find it for you.

My "research," reflecting my level of interest, has been limited to what I could find through Google. I was not able to find a copy of the Agreement from any year. For someone with a higher level of interest, a FOIA request should turn up everything that is available at minimal expense.

The problem is, we cannot assume anything. There was in 1963 an Agreement, a Code of Federal Regulations, a Federal Reserve Regulation J, a variety of operating circulars, and some standard procedure for processing PMOs at the level of the local bank, the Federal Reserve (as agent for the Postal Service) and the Treasury Department. We need to establish what the reality was.

The Gospel of Endorsements has been predicated almost entirely on a supposed "Wilmouth statement" that is looking more and more like a fabrication by John Armstrong, the God of Money Order Fakery. I seem to be the only one who finds the apparent fabrication and certainly the lack of explanation by Armstrong to be troubling (a lack of interest which I, in turn, find rather troubling and telling).

The 1960 FRB circular stated, "and with respect to matters not coveredby such agreement, the provisions of Regulation J, this circular and our time schedules shall be deemed applicable to all postal money orders." This seems like rather odd language to use if the Agreement were "published in operating circulars" as you suggest. I don't feel a burden to "prove you wrong" because you are simply making an assumption that is, on its face, inconsistent with the FRB circular.

On this thread, this forum, and all places where True Believers congregate, there is seldom anything resembling an effort to arrive at the actual truth. Various species of Young Earth Creationists, Radical Jihadists, New Atheists and Armstrong Groupies rabidly defend their turf, shouting down any evidence that challenges their position while being willing to make unlikely inferences and assumptions if this will prop up their position. It's what litigation would be like if we had no ethical rules, rules of evidence, rules of procedure, burdens of proof, presumptions, requirements for qualifying expert witnesses, etc. It would be utter chaos. If the truth actually did emerge by dumb luck, it would be lost in the chaos. To borrow a phrase from no less a philosopher than Mr. T, I pity the poor fool who doesn't understand why threads like this go nowhere.

Someone beat me to the punch of pointing out that the Armstrong sycophants have managed to derail the thread with the reliable changing-the-subject ploy. Yawn.

Hi Lance,

That was me that pointed out the attempt to change the subject.

Did you notice the point I made in post 319 (and before that in post 309) that what Sandy Larsen provided says the money order only needs to be endorsed TO THE ORDER OF any bank, not BY the bank? And that the current money order appears to meet that specified criteria, as it is endorsed via that Klein's stamp PAYABLE TO THE ORDER OF THE FIRST NATIONAL BANK OF CHICAGO?

http://educationforum.ipbhost.com/index.php?showtopic=22439&p=320774

I'm of the persuasion that pretty much seals the deal, unless something new comes up.

Hank

-

"The "bleed-thru" of the ink is a strong indication that postal money order 2,202,130,462, shown as CE 788, was not original card stock." -- John Armstrong

"I mean the bleed through. I don't see how it can be ignored. It really does seem to me to be a big faux pas, one which the WC apparently swallowed. I mean can someone explain it innocently?" -- James DiEugenio

In neither case did the person say anything had been proven.

Right on the Armstrong website the following statement is made regarding the bleed-thru:

"NOTE: Serious researchers should be focusing attention on the inked postal stamps that appear on the front of the money order (Dallas, TX, Mar 12, 1963), the inked endorsement stamp (Klein's) and the inked initials and dates that appear on the back of this money order. An explanation is needed as to how ink from the postal stamp and ink from the initials/dates can "bleed" thru to the other side of the money order. Postal money orders were made from card stock similar to an index card or an IBM type punch card--between 90# and 110# paper. This paper stock was crisp, firm, and ink "bleed-thru" to the reverse side was virtually impossible. I don't understand why or how ink "bleed-thru" occurred on CE 788. The original postal money order disappeared long ago, and only FBI photographs of CE 788 remain. Who authorized and/or caused the disappearance of the original money order is unknown. Only black and white photographs remain. This ink "bleed-thru" deserves a valid explanation."

Armstrong said, "This ink 'bleed-thru' deserves a valid explanation." And now we have it.

No claim was made by Armstrong other than the bleed-thru appearing to show that CE 788 was not original card stock.And the claim was factual at the time.

Armstrong obviously didn't research this very well, or else he would have discovered the answer in the Warren Commission testimony, as cited previously here by DVP, wouldn't he?

There's the rub. I see a lot of allusions to Armstrong's research, but if he couldn't even discover why there was bleed through, then that calls into question how great a researcher he really is.

Doesn't it?

Hank

The paragraph about ink bleeding on the money order isn't in Armstrong's book. It does appear on his website, clearly as an afterthought. And if you read the paragraph you will see that he doesn't claim to have researched it, because he urges "serious researchers" to do so.

The quote I saw was:

"The "bleed-thru" of the ink is a strong indication that postal money order 2,202,130,462, shown as CE 788, was not original card stock." -- John Armstrong

That is wrong.

Right?

Hank

-

More evidence the FBI falsified its own reports:

Hi Jim,

The subject of this thread is different than the subject you're trying to change it to.

That's a LOGICAL FALLACY known as a red herring (AKA "changing the subject").

Let me explain: http://www.nizkor.org/features/fallacies/red-herring.html

Fallacy: Red Herring

Also Known as: Smoke Screen, Wild Goose Chase.

Description of Red Herring

A Red Herring is a fallacy in which an irrelevant topic is presented in order to divert attention from the original issue. The basic idea is to "win" an argument by leading attention away from the argument and to another topic.

This sort of "reasoning" has the following form:

1.Topic A is under discussion.

2.Topic B is introduced under the guise of being relevant to topic A (when topic B is actually not relevant to topic A).

3.Topic A is abandoned.

This sort of "reasoning" is fallacious because merely changing the topic of discussion hardly counts as an argument against a claim.

Examples of Red Herring

•"We admit that this measure is popular. But we also urge you to note that there are so many bond issues on this ballot that the whole thing is getting ridiculous."

•"Argument" for a tax cut:

"You know, I've begun to think that there is some merit in the Republican's tax cut plan. I suggest that you come up with something like it, because If we Democrats are going to survive as a party, we have got to show that we are as tough-minded as the Republicans, since that is what the public wants."

•"Argument" for making grad school requirements stricter:

"I think there is great merit in making the requirements stricter for the graduate students. I recommend that you support it, too. After all, we are in a budget crisis and we do not want our salaries affected."

-

Deleted duplicate post

-

Endorsements

13. All cash items sent to us, or to another Federal Reserve Bank

direct for our account, should be endorsed without restriction to the

order of the Federal Reserve Bank to which sent, or endorsed to the

order of any bank, banker or trust company, or with some similar

endorsement.

Endorsed to the order of any bank...

The Money Order in question has that...

It reads:

PAY TO THE ORDER OF

THE FIRST NATIONAL BANK OF CHICAGO

50 91144

KLEINS SPORTING GOODS, INC.

So it appears you proved the money order has the correct stamp, and all is in good order.

Hank

REMINDER:

The above originally appeared in post #309 in this thread.

Hank

Hank,

Bingo!

Thank you for presenting this to us in such an easy to understand way.

--Tommy

Nonsense. There is no mark or endorsement of any kind from the First National Bank of Chicago, which there should be. Nor is there a mark or endorsement from the district FRB or national FRB. No one has ever said there was no rubber stamp appearing to be from Kleins on the money order. That is obvious.

Nonsense. yourself.

The quote says "... or endorsed TO THE ORDER OF any bank", Jim.

And we have that.

PAY TO THE ORDER OF

THE FIRST NATIONAL BANK OF CHICAGO

50 91144

KLEINS SPORTING GOODS, INC.

It is endorsed TO THE ORDER OF the First National Bank of Chicago.

There is nothing in the specifications provided that says it needs anything further. Your statement that "there should be" an "endorsement ... FROM the First National Bank of Chicago" (as opposed to "TO" the bank) is nowhere to be found in those specifications. [emphasis added throughout]

Simply repeating erroneous information doesn't make it more true.

Sandy Larsen provided the documentation that established the endorsement from Kleins TO THE FIRST NATIONAL BANK OF CHICAGO is all that is required. (Thanks, Sandy!)

Hank

-

Endorsements

13. All cash items sent to us, or to another Federal Reserve Bank

direct for our account, should be endorsed without restriction to the

order of the Federal Reserve Bank to which sent, or endorsed to the

order of any bank, banker or trust company, or with some similar

endorsement.

Endorsed to the order of any bank...

The Money Order in question has that...

It reads:

PAY TO THE ORDER OF

THE FIRST NATIONAL BANK OF CHICAGO

50 91144

KLEINS SPORTING GOODS, INC.

So it appears you proved the money order has the correct stamp, and all is in good order.

Hank

REMINDER:

The above originally appeared in post #309 in this thread.

Hank

-

"The "bleed-thru" of the ink is a strong indication that postal money order 2,202,130,462, shown as CE 788, was not original card stock." -- John Armstrong

"I mean the bleed through. I don't see how it can be ignored. It really does seem to me to be a big faux pas, one which the WC apparently swallowed. I mean can someone explain it innocently?" -- James DiEugenio

In neither case did the person say anything had been proven.

Right on the Armstrong website the following statement is made regarding the bleed-thru:

"NOTE: Serious researchers should be focusing attention on the inked postal stamps that appear on the front of the money order (Dallas, TX, Mar 12, 1963), the inked endorsement stamp (Klein's) and the inked initials and dates that appear on the back of this money order. An explanation is needed as to how ink from the postal stamp and ink from the initials/dates can "bleed" thru to the other side of the money order. Postal money orders were made from card stock similar to an index card or an IBM type punch card--between 90# and 110# paper. This paper stock was crisp, firm, and ink "bleed-thru" to the reverse side was virtually impossible. I don't understand why or how ink "bleed-thru" occurred on CE 788. The original postal money order disappeared long ago, and only FBI photographs of CE 788 remain. Who authorized and/or caused the disappearance of the original money order is unknown. Only black and white photographs remain. This ink "bleed-thru" deserves a valid explanation."

Armstrong said, "This ink 'bleed-thru' deserves a valid explanation." And now we have it.

No claim was made by Armstrong other than the bleed-thru appearing to show that CE 788 was not original card stock.And the claim was factual at the time.

Armstrong obviously didn't research this very well, or else he would have discovered the answer in the Warren Commission testimony, as cited previously here by DVP, wouldn't he?

There's the rub. I see a lot of allusions to Armstrong's research, but if he couldn't even discover why there was bleed through, then that calls into question how great a researcher he really is.

Doesn't it?

Hank

-

Anonymous tipsters play an incredibly important role on 11-22 and 11-23-63 re the rifle.

They are grossly under-appreciated by JFK researchers.

They are co-conspirators who helped greatly to frame Marina's husband.

One can learn a lot from the fact that a tip was called in anonymously.

For example, in the case of the money order, I think we learn from the anonymous tip on the supposed scope mounting at Irving Sports Shop that the FBI wasn't on the same page as the assassination conspirators. The FBI was supposed to have "discovered" that the scope had been mounted there. But their premature announcement, that they had found the order for the rifle and that it showed the price to be $12.78, bungled that plan.

This, among other things, tells me that those in the FBI weren't colluding with the conspirators in the CIA. The cover-up was separate from the assassination plot.

Or, we can learn that Dial Ryder wanted his coattails attached to the Kennedy Assassination as a historic footnotes, and got his 15 minutes of fame and then some. Please tell me the evidence that Ryder himself didn't call in that anonymous tip.

Hank

-

You REALLY can't figure this out, Jim?

I think it's fairly clear that the FBI just simply didn't release the EXACT DOLLAR AMOUNT ($21.45) that appeared on the front of the money order. So the media people were going with the CURRENT Nov. '63 price for the gun (without the scope)--$12.78.

But we know the FBI and Secret Service--on Nov. 23!--had the info regarding the exact dollar amount ($21.45), because CD75 and CD87 that I've linked dozens of times in this thread verify that fact.

So why would you think anything is "magic" or suspicious about this at all? Do you think BOTH of those documents (CD75 & CD87)---which are from TWO different agencies (the FBI and the SS)---are fake documents?

You're right, David, I can't figure out why you're speculating so wildly here.You want us to believe that the FBI released information about the magic rifle the day after the assassination, including the date of purchase, the vendor, and a handwriting analysis of the alleged orderer, and the fact that the orderer used an alias, but that it then withheld the price of the rifle so that news media all across the country could GUESS what the price might have been. AND you want us to believe that all the different reporters were completely wrong about the price, but came up with the EXCAT SAME INCORRECT PRICE, even though THREE DIFFERENT PRICES were shown just in the three or four little ads you entered into this thread. Not only that, but EVERY SINGLE REPORT I've seen failed to point out that the list price, often presented in the same paragraph as the rest of the information that could only have come from the FBI, was a GUESS, a GUESS made on the basis of multiple prices advertised for the weapon. Despite your speculation, the best reading of this evidence is that the FBI on 11/23 indicated the rifle cost $12.78, just as all those news stories reported so confidently.Here's on thing that might have happened: Someone other than Dial Ryder put repair tag #18374 with Oswald's name on it on Dial Ryder's workbench in the Irving Sports Shop gun store near Dallas. The repair, according to the tag, was to "drill and tap" and "bore sight" something that belonged to "Oswald." And so someone at the the FBI felt it would be safe to indicate that "Hidell" purchased the rifle from Klein's at the cost without a scope, $12.78. But the Ryder story soon fell apart, and now the FBI had to make the $12.78 price go away. It was easy to make it vanish from FBI internal documents, but removing it from scores of American news reports was simply impossible.And so the tap dance began. Magic media reports, a magic money order, a magic rifle that fired magic bullets... enough magic to make Harry Potter blush!Dial Ryder's story didn't break until after the money order was found, as I understand it.

See his testimony. The first time the FBI interviewed him was 11/25/63. Ryder pegs it "as the day of the funeral of President Kennedy".

So you'll need another guess.

Hank

-

Postal money orders required bank endorsement stamps in 1963.

I wish to address a document brought up earlier by Lance Payette in this thread. The document, a "circular" issued by a Federal Reserve Bank (FRB) in 1960, states that postal money orders are to be treated by FRBs as "cash items." "Cash item" simply means that the FRB gives banks instant credit for the item -- there is no waiting period for the item to clear. Even checks are usually treated by banks as cash items. (Or so I've read.)

The circular, which was in effect in 1963, also states that cash items presented to an FRB for collection are required to have bank endorsement stamps.

This seemingly would mean, therefore, that postal money orders required bank stamps. However, as Lance pointed out, there is a clause in the circular stating that there is an agreement between the Postmaster General and Federal Reserve Banks, and that the agreement may have removed the bank endorsement requirement for postal money orders. (The only known evidence for this possibility being the Hidell money order.) I will hereafter refer to this agreement as "The Agreement."

It was therefore important to find The Agreement. Lance stated that he couldn't find it. Neither could I.

HOWEVER...

It occurred to me that there had to have been a way for banks to be informed of exactly what the FRB requirements were. This got me to searching the Code of Federal Regulations (CFR) and Uniform Commercial Code (UCC) for bank endorsement regulations. I found documents dated 1909, 1925, 1987, and 2001 stating that bank endorsements were required specifically on postal money orders. But the documents I found closer to the 1960s suffered the same problem as the circular that I'm writing about now. They state that postal money orders are treated as cash items, and that cash items require bank endorsements. But they leave open the possibility of The Agreement nullifying the bank endorsement requirement on postal money orders.

THEN...

Today I found something interesting. I found another 1960s era FRB circular which has an appendix specifically for postal money orders. Upon reading it, I realized that I had found The Agreement! Not necessarily the full agreement, but the parts of the agreement that bankers needed to be aware of when presenting checks to an FRB.

Suddenly everything became clear. The regulations I had been seeking had been in front of me the whole time! THE CIRCULARS! The circulars are what are used to inform banks what FRB requirements are! Not the CFR. Not the UCC. The circulars!

Then I felt stupid for not realizing this earlier.

I checked the FRB website to confirm my conclusion. On this page

https://www.frbservices.org/regulations/operating_circulars.html

it is stated

"Federal Reserve Financial Services are governed by the terms and conditions that are set forth in the following operating circulars."

So, when a bank wants to know what the FRB requirements are, they look them up in the circulars. Duh!

SOOOOO...

How do we know whether or not postal money orders require bank stamps? We just read the appropriate circular. And, if we want to know if The Agreement nullifies the bank stamp requirement, we look for THAT in the circular.

Now, recall the 1960s era circular I found with the appendix containing (the pertinent part of) The Agreement. It is Appendix B in this 1969 circular:

https://fraser.stlouisfed.org/docs/historical/ny%20circulars/1969_6370.pdf

The regulations given for postal money orders in this circular are pretty much the same as the regulations given in the 1960 circular that was in effect in 1963. But this one has The Agreement in Appendix B. Quoting from this document:

Items which will be handled as cash items

3. Except as otherwise provided by this operating circular, the

following items may be sent to this Bank for handling as cash items

in accordance with and subject to the provisions of Regulation J, of

this operating circular, and of our time schedules:

( a ) Checks drawn upon any bank included in the current “Federal

Reserve Par List,” which indicates the banks upon which checks are

collectible at par through the Federal Reserve Banks and is furnished

from time to time and supplemented each month to show changes sub

sequent to the last complete list.

( b ) Government checks, postal money orders, and food stamp cou

pons.*

( c ) Such other demand items, collectible at par in funds accept

able to the Federal Reserve Bank of the District3 in which such items

are payable, as we may be willing to accept as cash items.

*Provisions [i.e. The Agreement] governing the collection of the foregoing

cash items are contained in Appendix A, Appendix B, and Appendix C,

respectively, of this operating circular.

o

o

o

APPENDIX B

POSTAL MONEY ORDERS

1. Postal money orders (United States postal money orders;

United States international postal money orders; domestic-inter

national postal money orders) will be handled by us as cash items in

accordance with an agreement made by the Postmaster General, in

behalf of the United States, and by the Federal Reserve Banks as

depositaries and fiscal agents of the United States pursuant to authori

zation of the Secretary of the Treasury. With respect to matters no*t

covered by that agreement, the terms and conditions of Regulation J

applicable to cash items, of this operating circular, and of our time

schedules shall be applicable to all such postal money orders.

2. We will give immediate credit for postal money orders received

from a sender maintaining or using an account with us as provided

in our time schedules. Simultaneously with such credit, we will debit

the amount of such money orders against the general account of the

Treasurer of the United States under such symbol numbers as may

be assigned by the Treasurer of the United States; and such credit

to the account of the sender shall then become final as between us and

the sender.

3. The agreement between the Postmaster General and the Federal

Reserve Banks provides, in effect, that no claim for refund or other

wise with respect to any postal money order debited against the gen

eral account of the Treasurer of the United States and delivered to

the representative of the Post Office Department as provided in said

agreement (other than a claim based upon the negligence of a Federal

Reserve Bank) shall be made against or through any Federal Reserve

Bank; that, if the Post Office Department makes any such claim with

respect to any such money order, such money order will not be re

turned or sent to a Federal Reserve Bank, but the Post Office Depart

ment will deal directly with the bank or the party against which such

claim is made; and that the Federal Reserve Banks will assist the

Post Office Department in asserting such claim, including making

their records and any relevant evidence in their possession available

to the Post Office Department. Section 210.12 of Regulation J, relat

ing to the return of cash items by the paying banks, is not applicable to

postal money orders.

There is nothing in The Agreement about bank endorsements. But in the body of the circular is this clause:

Endorsements

15. All cash items sent to us, or to another Federal Reserve Bank

direct for our account, should be endorsed without restriction to, or

to the order of, the Federal Reserve Bank to which sent, or endorsed

to, or to the order of, any bank, banker, or trust company, or en

dorsed with equivalent words or abbreviations thereof. The endorse

ment of the sender should be dated and should show the A.B.A. transit

number of the sender, if any, in prominent type on both sides of the

endorsement.

So we see that bank endorsements were required on postal money orders. (No big surprise.)

But remember, these are 1969 regulations, not the 1960 ones that were in effect in 1963. The reason I quote them here is to reveal The Agreement, and also to show that the regulations were essentially the same in 1969 as they were in 1960 (and 1963).

But why wasn't The Agreement printed in the 1960 circular as it was in 1969? As it turns out, IT WAS! It just wasn't set apart in its own appendix.

Now I will quote from the 1960 circular:

https://fraser.stlouisfed.org/docs/historical/ny%20circulars/1960_04928.pdf

Items which will be accepted as cash items

1. The following will be accepted for collection as cash items:

(1) Checks drawn on banks or banking institutions (including private

bankers) located in any Federal Reserve District which are collectible

at par in funds acceptable to the collecting Federal Reserve Bank. The

“ Federal Reserve Par List,” indicating the banks upon which checks will

be received by Federal Reserve Banks for collection and credit, is fur

nished from time to time and a supplement is furnished each month

showing changes subsequent to the last complete list. This list is subject

to change without notice and the right is reserved to return without

presentment any items drawn on banks which may have withdrawn or

may have been removed from the list or may have been reported elosed.

(2) Government checks drawn on the Treasurer of the United States.

(3) Postal money orders (United States postal money orders; United

States international postal money orders; and domestic-international

postal money orders).

(4) Such other items, collectible at par in funds acceptable to the

Federal Reserve Bank of the District in which such items are payable, as

we may be willing to accept as cash items.

o

o

o

Postal money orders

11. Postal money orders will be handled in accordance with

an agreement made by the Postmaster General, in behalf of the

United States, and the Federal Reserve Banks as depositaries and

fiscal agents of the United States pursuant to authorization of the

Secretary of the Treasury; and with respect to matters not covered

by such agreement, the provisions of Regulation J, this circular and

our time schedules shall be deemed applicable to all postal money

orders. Immediate credit will be given to member banks and non

member clearing banks for postal money orders as provided in our

time schedules and simultaneously with such credit we will debit the

amount of such money orders against the general account of the Treas

urer of the United States under such symbol numbers as may be

assigned by the Treasurer of the United States. Said agreement fur

ther provides in effect that no claim for refund or otherwise with

respect to any money order debited against the general account of

the Treasurer of the United States and delivered to the representa

tive of the Post Office Department as provided in said agreement

(other than a claim based on the negligence of a Federal Reserve

Bank) will be made against or through any Federal Reserve Bank;

that if the Post Office Department makes any such claim with respect

to any such money order, such money order will not be returned or

sent to a Federal Reserve Bank, but the Post Office Department will

deal directly with the bank or the party against which such claim is

made; and that the Federal Reserve Banks will assist the Post Office

Department in making such claim, including making their records

and any relevant evidence in their possession available to the Post

Office Department

o

o

o

Endorsements

13. All cash items sent to us, or to another Federal Reserve Bank

direct for our account, should be endorsed without restriction to the

order of the Federal Reserve Bank to which sent, or endorsed to the

order of any bank, banker or trust company, or with some similar

endorsement. Cash items will be accepted by us, and by other Federal

Reserve Banks, only upon the understanding and condition that all

prior endorsements are guaranteed by the sending bank. There should

be incorporated in the endorsement of the sending bank the phrase,

“ All prior endorsements guaranteed.” The act of sending or delivering a

cash item to us or to another Federal Reserve Bank will, however,

be deemed and understood to constitute a guaranty of all prior

endorsements on such item, whether or not an express guaranty is

incorporated in the sending bank’s endorsement. The endorsement of

the sending bank should be dated and should show the American

Bankers Association transit number of the sending bank in prominent

type on both sides.

As can be seen, The Agreement in this document is located in item #11, as opposed to a separate appendix.

THEREFORE...

Postal money orders required bank endorsement stamps in 1963.

Endorsements

13. All cash items sent to us, or to another Federal Reserve Bank

direct for our account, should be endorsed without restriction to the

order of the Federal Reserve Bank to which sent, or endorsed to the

order of any bank, banker or trust company, or with some similar

endorsement.

Endorsed to the order of any bank...

The Money Order in question has that...

It reads:

PAY TO THE ORDER OF

THE FIRST NATIONAL BANK OF CHICAGO

50 91144

KLEINS SPORTING GOODS, INC.

So it appears you proved the money order has the correct stamp, and all is in good order.

-

But at the moment I don't think that is what happened, because it appears to me that the money order was actually made on regular paper, not the real card stock. Because the ink has bled through all over the place. Why anybody would fabricate a money order on regular paper, I have no way of knowing. And it makes no sense to me. But that's what appears to have happened. I have a hard time believing that the bleed-thru that we see is actually due to the MO getting wet, as Lance notes has been suggested.

Actually, I can think of one reason why regular paper might be used. If the intention was to merely provide photographs to the authorities, not a real money order, using a photocopier to make the MO could be handy. It could be retouched and then photocopied again, and repeated if necessary. When finished, a photo is given to the WC.

If this were the case, one would have to explain how it was that somebody actually held and carried the MO from Alexandria, or wherever it was the MO came from. I don't know the details enough to determine if that was feasible.

This scenario requires that a photocopy machine would be able to reproduce bleed-through without also reproducing any evidence of touch-ups. Meanwhile, capillary action is a common phenomenon; card stock is permeable and fibrous; inks have many different levels of viscosity and density, and adding water changes their viscosity and density. I, for one, find the latter explanation more believable than the former.

I was thinking that the photocopy method would allow the handwriting forger to perfect Oswald's handwriting, and that everything else would be added last (after photocopying). But I just checked and even the Oswald handwriting bleeds through.

So I'm stumped.

The reason the bleed-through bothers me is that almost all the inks bled through, not just one or two. And my experience writing on various papers as a young person -- which was considerable -- tells me that the card stock would not bleed very easily. On the other hand, my experience was in the early seventies, not the early sixties. Perhaps there was significant change with inks or card stock between those two periods. (That's a little hard to accept because virtually nothing has changed since the early seventies and now. I still buy the same types of paper and card stock, and the same magic markers, Sharpie.)

Here's another possibility. The photocopy method was used. But the reason for doing so wasn't to re-copy and perfect the handwriting. The purpose was to allow numerous takes at creating the money order. So if the handwriting wasn't quite right, merely make another photocopy and try again. Once satisfied, apply the stamps.

Like you, I prefer the other explanation. But the bleed-through really bothers me. I hope that my tests on true card stock shows a lot of bleed-through... that would simplify things for me.

Isn't the original money order in the National Archives?

Wouldn't that save a lot of trouble and speculation if that was examined?

If the original money order is in the archives and it's on card stock and it's got bleed-thru, where's that leave us?

Hank

-

More dirt on the casket:

CHAPTER 7000 http://tfm.fiscal.treasury.gov/v2/p4/c700.html

PROCEDURES FOR PROCESSING POSTAL MONEY ORDERS

Appendix B – Processing Postal Money Orders

· Purchaser of the PMO designate a “Payee” and fills out the purchaser’s information

· Purchaser pays for the PMO – Postal clerk tears PMO from stub and hands to Purchaser

· Purchaser provides PMO to designated Payee for deposit in exchange for goods/services

· Payee endorses the back of the PMO and deposits PMO in their Bank

· The Bank will then PROCESS the PMO, adding whatever marks, electronic or otherwise to the back of the PMO and record the payment to Payee in their records

o The Bank, now the new Payee, forwards the PMO to their affiliated Federal Reserve Bank for reimbursement of funds and processing

3.0 Federal Reserve System

3.1General

All money orders are forwarded through the Federal Reserve Banking System, to which commercial banks have access.

3.2 Payment

The postmaster general has the usual right of a drawee to examine money orders presented for payment by banks through the Federal Reserve System and to refuse payment of money orders, and has a reasonable time after presentation to make each examination. Provisional credit is given to the Federal Reserve Bank when it furnishes the money orders for payment by the postmaster general. Money orders are deemed paid only after examination is completed, subject to the postmaster general’s right to make reclamation under 3.4.

3.3 Endorsement

The presenting bank and the endorser of a money order presented for payment are deemed to guarantee to the postmaster general that all prior endorsements are genuine, whether an express guarantee to that effect is placed on the money order. When an endorsement is made by a person other than the payee personally, the presenting bank and the endorser are deemed to guarantee to the postmaster general, in addition to other warranties, that the person who so endorsed had capacity and authority to endorse the money order for the payee.

3.4 Reclamation

The postmaster general has the right to demand refund from the presenting bank of the amount of a paid money order if, after payment, the money order is found to be stolen, or to have a forged or unauthorized endorsement, or to contain any material defect or alteration not discovered on examination. Such right includes, but is not limited to, the right to make reclamation of the amount by which a genuine money order with a proper and authorized endorsement has been raised. Such right must be exercised within a reasonable time after the postmaster general discovers that the money order is stolen, bears a forged or unauthorized endorsement, or is otherwise defective. If refund is not made by the presenting bank within 60 days after demand, the postmaster general takes such actions as may be necessary to protect the interests of the United States.

BTW, please note the last paragraph, the first sentence. If the PMO has no bank endorsement, if it turns out to be bogus or fraudulent, how could the FRB know who to get their money back from unless it was endorsed by a bank?

Doesn't the stamp on the back of the money order in question already satisfy those conditions?

It identifies the original payee, the bank it was deposited to, and the account number of the original payee.

PAY TO THE ORDER OF

The First National Bank of Chicago

50 91144

KLEIN'S SPORTING GOODS, INC.

Why would they need an additional stamp by the bank itself for the FRB to know where it came from?

All that info's already there.

-

Sorry if this is a stupid question. What does the stamp on the back mean? I try to think of something. Is not the

PAY TO THE ORDER OF

The First National Bank of Chicago

50 91144

KLEIN'S SPORTING GOODS, INC.

where the numbers are an account number and the name the name of the account? Maybe in being stamped with the words of a disbursement money order it signifies as having re-entered the postal system which means as far as the account holder is concerned it has been paid?

edit clarification, typos

dited by John Dolva, Today, 11:20 AM.

"And see page 211, section 762.11a: "Disbursement Postal Money Orders have words of negotiability -- "Pay to the Order of" -- printed on their face, while other postal money orders simply bear the words "Pay to" on their face."" - a postal money order converted to an internal disbursement money order by being stamped on the back?

A disbursement money order issued by the postal service is to pay their own bills, John.

Consumer money orders are different. They are sold to consumers who want to mail money through the mail (to purchase something or pay their own bills) but who may not have access to a checking account.

You don't convert a consumer money order into a disbursement money order by stamping 'pay to the order of' on the back, front, or any of the four edges.

Oswald wasn't trying to pay the post office's bills and neither was Kleins. Oswald was trying to buy a rifle when he purchased that money order, and Kleins was trying to get the money into their account when they cashed it.

Please go back and read the sections cited by me and posted here by David Von Pein about what disbursement money orders are, and are not.

http://educationforum.ipbhost.com/index.php?showtopic=22439&page=10#entry319457

Specifically, this:

A disbursement money order is one the Post Office issues to pay its own bills... they disburse the money to various contractors who do repairs, or those who they buy stuff from.

See the prior page, section 762.13: "Disbursement Postal Money Orders are issued solely by Postal data centers and solely for the purpose of paying Postal Service obligations."

Also see that page, section 762.11b: "Disbursement Postal Money Orders, unlike other postal money orders, bear on their face the phrase, "This special money order is drawn by the postal service to pay one of its own obligations"."

And see page 211, section 762.11a: "Disbursement Postal Money Orders have words of negotiability -- "Pay to the Order of" -- printed on their face, while other postal money orders simply bear the words "Pay to" on their face."

and this, which I didn't bother to quote (added by DVP):

762.11c --- "The amounts of Disbursement Postal Money Orders are printed in words as well as numbers, while the amounts of postal money orders available at post offices are printed in numbers only."

Hank

Yes, postal money orders do require bank endorsements!

in JFK Assassination Debate

Posted · Edited by Hank Sienzant

All these steps are part of one transaction.

Nobody is disputing that. In fact, it's good of you to finally admit it. You've been arguing all along these are not all part of one transaction, haven't you?

So to say for example, that the processing of my charge card is not related to signing the receipt--I mean who the heck buys that baloney? You are the one passing out red herrings.

That's the LOGICAL FALLACY of a straw man argument. I didn't say they were unrelated... I said it was a change of subject to start talking about the bullet or the rifle when the subject of this discussion is the money order, and only the money order. In one sense, if you step far enough back, everything is related, so you can change the subject from Oswald's supposed fluency in Russian to the paper bag found on the sixth floor, and argue that those are related. But when we're discussing the paper bag, to switch to talking about Oswald's fluency in Russian is a change of subject. And so is switching to talk about the rifle when the subject of the thread is the money order. And here's the subject of the thread, Jim:

Yes, postal money orders do require bank endorsements!

http://www.nizkor.org/features/fallacies/straw-man.html

Description of Straw Man

The Straw Man fallacy is committed when a person simply ignores a person's actual position and substitutes a distorted, exaggerated or misrepresented version of that position. This sort of "reasoning" has the following pattern:

1.Person A has position X.

2.Person B presents position Y (which is a distorted version of X).

3.Person B attacks position Y.

4.Therefore X is false/incorrect/flawed.

This sort of "reasoning" is fallacious because attacking a distorted version of a position simply does not constitute an attack on the position itself. One might as well expect an attack on a poor drawing of a person to hurt the person.

You have been hanging out at McAdam's' place too long. What happens is you end up like him.

And you're still resorting to the LOGICAL FALLACY of poisoning the well.

He still can't figure rout what he did wrong with Cheryl Abbate.

And there's the LOGICAL FALLACY of the red herring once more.

Can't discuss the money order? Change the subject! Start discussing the rifle, or CE399, or Cheryl Abbate.

Hank